If you run a business in a high‑chance enterprise like CBD, adult, gaming, tour, or subscription offerings, you’ve probably heard about high‑hazard service provider accounts. These money-owed allow groups which standard processors might frequently reject to accept credit cards, ACH, and eCheck payments.

What Makes a Merchant “High Risk”?

“High‑risk” doesn’t always mean illegitimate; it simply manner certain traits make payment processors extra careful. Typical danger factors encompass:

Industries with higher chargeback or fraud chance include grownup leisure, CBD/hemp, online gaming and gambling, travel, ticketing, subscription-primarily based services, nutraceuticals, forex/crypto, virtual items, and more. Businesses with recurring billing or subscription cycles, in which customers may forget about or dispute expenses.

High average transaction size or international income/worldwide transactions may also increase fraud or disputes. Poor credit history, limited processing history, or volatile sales both for the enterprise and its owner(s).

Because of those elements, fee processors see a greater threat of chargebacks, fraud and losses, which results in stricter underwriting, better fees, and further safeguards for excessive‑threat merchant accounts.

How High-Risk Merchant Accounts Work (and What They Offer)

A high-risk merchant account (or high-risk payment gateway) gives charge processing services tailored to corporations with accelerated threat. Key functions:

- Accept credit score cards, debit playing cards, ACH / eCheck, and every now and then opportunity payment methods.

- Provide fraud prevention gear, chargeback management, and threat tracking to reduce the probability of disputes or losses.

- Offer a global payment processing/multi-forex guide, enabling merchants to sell the world over.

- When permitted, allow merchants to perform regardless of “terrible credit” or threat-heavy commercial enterprise fashions.

These capabilities make excessive‑risk fee processing a viable lifeline for companies that mainstream processors (like commonplace gateways) refuse or limit.

Pros and Cons of High-Risk Merchant Accounts

Pros:

- Payment gets admission to: Accept payments in restricted industries like CBD, person, gaming, journey, and subscriptions.

- Global attain: Multi-currency and worldwide payment aid for scaling income.

- Fraud & chargeback tools: Protection via fraud detection, chargeback mitigation, and dispute decision.

- Integration options: Support for credit cards, ACH/eCheck, subscriptions, and habitual billing.

Cons:

- Higher expenses: Includes transaction, month-to-month/gateway, and chargeback charges.

- Stricter approval: More documentation, credit score exams, and compliance requirements.

- Account hazard: The Possibility of closure or regulatory scrutiny if issues arise.

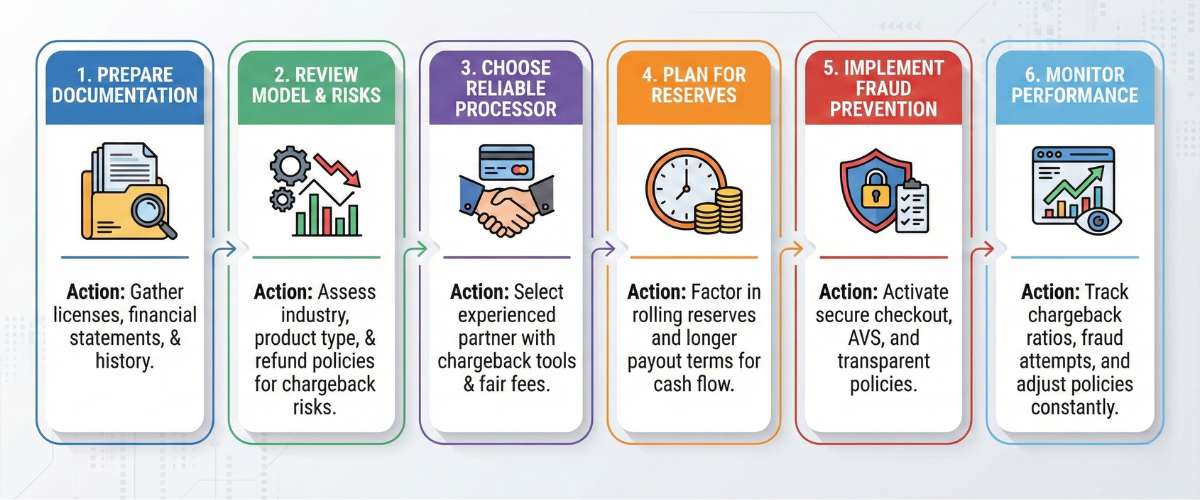

Step‑By‑Step: How to Get Approved for a High-Risk Merchant Account

If you watched your business qualify and you’re prepared to use it, right here’s what you must do to maximise your chances:

- Prepare documentation: Have ready enterprise licences, financial institution statements, economic history, evidence of commercial enterprise operations, and perhaps owner credit records if required.

- Review business model & risk areas: Understand how your industry, product type, pricing, refund/return coverage, and customer base might affect chargeback or fraud danger.

- Choose a reliable high-risk fee processor: Look for one with revel in on your industry, a good reputation, chargeback management gear, an international charge guide, and fair, not exorbitant expenses.

- Expect and plan for rolling reserves / longer payout terms: Factor in coin float delays when making financial projections.

- Implement fraud prevention and compliance measures: Use first-rate practices, stable checkout, correct product descriptions, transparent refund policies, deal with verification (AVS), CVV assessments, and habitual‑billing transparency if applicable.

- Monitor your overall performance constantly: Track chargeback ratios, fraud tries, client lawsuits, transaction volumes, and alter regulations to lessen risks over time.

Hidden Costs & Risks

Before you jump in, make sure you understand the full cost structure and long-term risks of high-risk payment processing:

- Transaction fees, per‑transaction fees, monthly gateway or maintenance fees: Often higher than standard accounts.

- Reserve requirements or upfront deposit: Some processors may demand upfront sums or withhold part of your sales flow.

- Chargeback fees and dispute handling fees: Each chargeback might cost $20–$100, and frequent disputes can trigger account review or termination.

- Delayed payouts or volume caps: Some providers limit monthly volume or delay payout schedules, which can impact cash flow or growth.

- Stringent compliance and documentation demands: Especially for regulated industries (adult, CBD, gambling, travel), non-compliance can result in account freeze or closure.

Also Read: GE Universal Remote Codes

How to Minimize Risk & Keep Payment Processing Healthy

Having a high-risk merchant account isn’t a guarantee of success depends on how well you manage risk. Here are proven strategies:

- Maintain low chargeback ratios: Aim for underneath 1% chargeback ratio (or something threshold your processor units), as frequent disputes are the main cause for account closure.

- Implement robust fraud prevention: Use address verification (AVS), CVV tests, steady checkout, tokenization, and fraud‑detection equipment. Limit suspicious transaction styles (e.g. large quantities, many orders from the same IP, common global orders).

- Have clear refund and delivery rules: Transparent, patron‑pleasant regulations lessen disputes and chargebacks.

- Diversify charge options: Offer credit/debit cards, ACH/eCheck, and likely opportunity price strategies. This spreads threat and gives flexibility.

- Keep accurate records & comply with regulations: For regulated industries, stay updated on licensing, compliance, data protection, and KYC/AML obligations.

FAQs

Q1: What is an excessive-risk merchant account?

A payment account for groups with better threat, like high chargebacks, regulated industries, or massive/worldwide transactions.

Q2: How long does approval take?

Usually some days to numerous weeks because of stricter assessments.

Q3: Can a business with awful credit get authorised?

Yes, in case you provide the specified documentation and are clear about your enterprise.

Q4: What fees are you worried about?

Higher transaction costs, month-to-month/gateway costs, chargeback expenses, and occasionally a rolling reserve.

Conclusion

High-risk merchant debts offer a vital lifeline to groups that mainstream processors frequently reject, enabling price acceptance, global reach, and bendy fee techniques. But these blessings include alternate‑offs: higher fees, rolling reserves, compliance burdens, and the continuing requirement to manipulate fraud and chargebacks carefully.